Will Blockchain Technology Destroy Your Small Business?

Given all the recent hype, it’s likely that you’ve been hearing a lot about Bitcoin and the blockchain technology upon which it is based.

As with any “new,” [Bitcoin’s been around since 2009, but is getting a huge amount of press now] little understood technology [think robots], there’s a tendency to paint it in a negative light and ask questions about its power to destroy what we hold near and dear – in this case, our small businesses.

Before we speculate too much on any good or bad that may come of blockchain technology, let’s take a moment to understand what it is. Remember, this is a very basic overview.

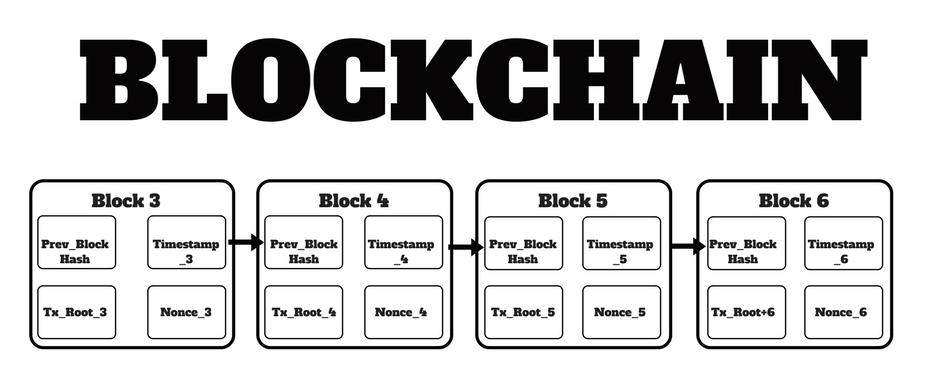

A blockchain is, as its name would imply, a chain of blocks.

What is contained in these blocks, you may ask?

To understand what’s contained in the blocks, let’s take a closer look at Bitcoin, which is the most famous manifestation to-date of blockchain technology. Forget, for a moment, all the hype around Bitcoin and the resulting massive fluctuations in its value. We can save that for a later conversation. For now, we’ll just consider what is contained in the blocks of the Bitcoin blockchain.

Each block of the Bitcoin blockchain, as depicted in the graphic at the beginning of this article, contains a series of transactions that have been cryptographically secured and which have been validated by a process called mining. The way the data is secured and the way the blocks are mined go beyond the scope of this article, but if you’re interested in further details, let me know and I’ll either write additional articles on this topic, or point you in the direction of some good resources.

So, back to the transactions that are included in the blocks of the Bitcoin blockchain. These transactions could include instances where you or I purchased something of value from a vendor and paid for it with Bitcoin, as well as a number of other unrelated transactions – usually around 2,000 transactions per block, at the present time.

For such a transaction to take place, we, as the buyer, would typically have Bitcoin in a “virtual” wallet. We would then instruct the wallet to send a certain number of Bitcoins to the vendor in order to pay for whatever we were buying. The transaction would be recorded as a certain amount of Bitcoin being moved from our virtual address to the virtual address of the vendor.

So, how is this different than just paying the vendor with Paypal, or with any credit card, you may ask?

On the surface, you as the consumer, and the seller as the vendor really shouldn’t see much difference. In theory, though, there are many differences between using blockchain-based Bitcoin and just using a credit card. A few of the more important differences in the context of this discussion are:

Anonymity: given that what’s recorded in the transaction and included in the blockchain is just a transfer of Bitcoin between two addresses, there is the (supposed) benefit of anonymity.

In reality, though, it’s pseudonymity, because if you want to transmit or receive value that translates to the real word, you’ll have to be connected to the virtual address or pseudonym somehow.

And the reality is, it’s been proven that with enough time and resources, even if you use different pseudonyms, and even mixing of those pseudonyms for every transaction, given that the Bitcoin blockchain is public, an attacker or “adversary” with enough time and resources can often break the pseudonym and connect the transactions with real-world identities.

So, those who would use Bitcoin (or other, similar cryptocurrencies) for nefarious and/or illegal purposes, are in for a rude awakening, if they get high enough up on the law enforcement priority list – see the Silk Road Marketplace case for an example.

Irreversible: once the transaction is in the blockchain, you as the buyer, or the vendor as the seller, cannot rewrite history. That is to say, once the transaction has been confirmed through the “mining” process and is included in the blockchain beyond the point where it could theoretically be reversed by a “51 percent” or “double spend” attack (again, beyond the scope of this article, but an attack where a miner(s) with a large enough percentage of the computing power on the network tries to commit fraud and “rewrite history”), it is there forever and cannot be changed without the agreement of both parties to the transaction.

Even it were to be changed or reversed, that would be done in a separate and subsequent transaction; the original transaction would still be in the blockchain with a (virtual) timestamp relative to the timing of other transactions in the chain.

Transparent: As stated above, what happens in the Bitcoin blockchain stays in the blockchain, but not only does it stay there, it’s there for all to see. Given that the Bitcoin blockchain is public, unlike when you do a transaction with Paypal or with a credit card, that transaction is out there for all to see. Again, they’ll only be able to associate the transaction with you if they know your public/virtual (key) identity, either because you give it to them or they figure it out by inference or other means. This transparency could be seen as a pro or a con of the blockchain, depending on where you sit and what you’re trying to accomplish.

These are just a few of the differences between doing a transaction with a standard payment method such as Paypal or a credit card, but they start to give you a sense of what’s stored in the blockchain and what’s different about a blockchain-based cryptocurrency such as Bitcoin.

Let’s change gears for a moment and talk about blockchain technology in a context other than that of a cryptocurrency like Bitcoin.

As you can see from the Bitcoin example above, the blockchain is essentially a way to create, execute, and store transactions, in indelible ink, so to speak, so that they are: 1.) (somewhat) anonymous, if desired; 2.) irreversible; and 3.) can be seen by all who have access to the blockchain in question.

So, given these characteristics, another useful way to think of the blockchain, is as a distributed or shared ledger.

One thing we didn’t touch on in the Bitcoin example is that the blockchain typically, but not necessarily, is shared across all nodes in the network. That is, every server on the network where the blockchain is stored has a full and complete copy of the blockchain and therefore, of all transactions that have ever been confirmed and included in any block that forms part of the blockchain.

If you think about that for a moment, it is in stark contrast to the way data is usually stored. Usually, data is stored on a central server, then those who need or want access to that data access the central server (sometimes without permission) and use whatever they’ve accessed for the purpose at hand.

In contrast, with blockchain technology, on a shared or distributed ledger, there are complete copies of the data (all the data, since the blockchain started) on several, perhaps thousands of nodes (servers). This is quite different and can only be accomplished because of the cryptographic nature of the way the transactions are included, confirmed and stored in the blocks. In that sense, it has the potential to be quite revolutionary for many data-based aspects of business.

It also tends to bog down and can be quite slow – another topic beyond the scope of this article – but many believe that some of the characteristics mentioned above make the blockchain approach worth some of the speed trade-offs. There is also hope that as time goes on and the technology progresses, the speed trade-offs relative to centrally managed and controlled networks will not be as pronounced.

Well, that’s probably more than enough to overwhelm you for now.

I will conclude here by saying that, in my opinion, blockchain technology certainly will not destroy most of your businesses! In fact, I believe that it has the potential to be revolutionary, in a positive way, in how many aspects of today’s businesses are run, but I will save that discussion for another time.